Read the this article. Trudeau and Freeland seriously screwed up the Canadian Banking System when they announced and subsequently bragged about freezing bank accounts and going after associated crypto accounts. You can’t do this type of action unless there is co ordination of all world banking systems or one world bank. Cash is being withdrawn and it’s probably continuing.. most likely, they got a rude awakening and even scolded privately by international bankers, WEF, IMF etc. They created a contagion of non confidence in banking that has probably spread to banking systems throughout the world. They seriously damaged the plans for implementation of digital IDs worldwide by freezing accounts arbitrarily.. bank runs in Canada will probably continue.. Watch out.. gold and silver will go through the roof.

I do not know how serious this is going to be. But I can tell you this:

A TD bank employee mentioned that her superior talked about the problems with Trudeau’s action in freezing bank accounts. My contact at TD Wealth Management told me that there are talks of some people cashing out.

The day after Trudeau froze bank accounts, TD, RBC, BMO and Scotiabank reported outages:

Why did they have outages? Was it due to a high traffic of customers withdrawing cash?

If you understand how banking works, which is based on fractional banking, 100% of the depositors need to withdraw only 10% of their money and there will be a bank run and banks will be in serious trouble.

Yesterday, my neighbour told me that two of his friends were donors to the Freedom Convoy at GiveSendGo and were doxed by the criminal hacker. One of his friends had to contact the bank every time he wanted to use his credit card. I can almost guarantee you that every donor to GiveSendGo will be withdrawing 10% or more of their money, now that their bank accounts are unfrozen. However, 10% of Canadians did not donate to GiveSendGo. But a percentage of Canadians and foreigners, who did not donate, will withdraw some money from the banks, just in case the government freezes their accounts for another reason.

Then there is negative media coverage from outside Canada:

Wall Street Journal: Justin Trudeau’s Liberal Tyranny Ottawa is now freezing bank accounts as if the truckers are terrorists.

U.S. venture capitalist David Sacks is the founding COO of PayPal. In a write-up for Common Sense, a newsletter curated by former New York Times columnist Bari Weiss, Sacks warned that Canada’s “dystopian” usage of the Emergencies Act to freeze bank accounts without oversight could be a preview of coming attractions for the United States. “It’s a Western version of China’s social credit system that does not altogether prohibit political dissent but makes it so costly that it becomes impractical to the ordinary citizen,” he wrote.

Matt Taibbi, the political columnist for Rolling Stone, wrote on his Substack that Canada was on the fast track to “bureaucratic dystopia.” Titling the column “when boring people turn dangerous” he took particular aim at Canadian Finance Minister Chrystia Freeland who, like Taibbi, was an expat journalist in 1990s Russia. Decrying the “sci-fi” dystopianism of her Emergencies Act orders against the financial system, Taibbi repeated an anti-Freeland slam coined by one of her former foreign correspondent contemporaries: “The Nurse Ratched of the New World Order.”

Man, Justin Trudeau is just being destroyed by American media, and it's not just @FoxNews.

The New York Times was one of the more surprising foreign publications to throw in their lot with the truckers – or at least, the truckers’ right to protest. “We disagree with the protesters’ cause, but they have a right to be noisy and even disruptive,” wrote the Times editorial board. As a publication whose reporters are constantly at the front lines of demonstrations around the world, the Times also threw cold water on the notion that a few thousand truckers were somehow a threat to Canadian democracy. “By the standards of mass protests around the world, the ‘Freedom Convoy’ snarling Downtown Ottawa ranks as a nuisance,” they wrote.

Will Americans, Asians or Europeans hesitate to invest in Canada, for fear of not being able to get their money out? Most likely, a percentage of them will.

There is definitely a hit to the confidence of the Canadian government and Canadian banks.

The financial sector is the biggest sector in Canada and the TSX. (The biggest sector in the U.S. is technology.) The banks are instrumental to a healthy economy. Businesses need financing to fund growth or maintain existing operations. Consumers need financing to spend on homes and merchandise. If there is an impediment on this, it will affect the economy. Therefore, this is bearish on Canadian stocks. Diversifying your investments away from Canada would be very prudent right now.

One of my close friends told me that investors are leaches and that they do not create any value.

It makes me wonder how many people believe this. I guess it’s possible that many do. I agree that there are people who make money from stocks and do not create much value. I think these are people on the gambling side who are not really investing. These are people who day-trade or play options.

So, do investors create value and how?

I think that most people would agree that entrepreneurs create value, by creating new goods and services. Thomas Edison created value by creating light bulbs which replaced gas lanterns. Henry Ford created value by creating cars, which replaced horse buggies. Elon Musk created value by creating electric cars, which will replace gas cars. Steve Jobs created value by creating the smart phone.

There are now thousands of companies creating value by creating new products and services. They range from planes to solar panels to computers to yoga clothing. Most of them needed investors to start. Yes, investors. Even the entrepreneur who started the company is an investor. Edison, Ford, Musk and Jobs were investors. The entrepreneur invested time and money to start the company. Time is essentially money, because if the entrepreneur did not spend the time to start a company, he/she could have spent the time to work at a job to earn income. Then the entrepreneur usually needs to get additional investors, starting with friends and family, then angel investors and then venture capitalists. This is because the company needs investments to fund growth. It needs the money to pay for R&D to create products, or to pay for marketing and operations. It gets this money by selling shares to investors. If these companies succeed, nobody would argue that everyone involved in creating the company has created value.

Investors usually take huge risks by investing in startup companies. The far majority of startups fail, consequently, investors lose money on most investments. So, when the few companies succeed, investors should be rewarded handsomely to compensate for the other losses, otherwise nobody would be willing to take the risk of investing in startup companies. The reward/risk ratio needs to make sense and entice investors to invest in companies, otherwise no company would get created.

Rarely does a company stop needing investments to fund growth. If the company becomes big enough, it goes public by getting listed on a stock market, in order to get even more investment. It gets this money by selling shares to “retail” investors in the public.

Many people might think that the stock market’s main purpose is for investors. Not necessarily. It was originally created to enable companies to raise money from investors. Companies need the stock market just as much as investors. In other words, companies need investors.

Quite often, countries work hard to attract foreign investment. They do this because they know that investors help create or grow companies, and companies create value in many ways: products, services, jobs, tax revenue, etc.

Usually investors take money that they earned from years of salaries and invest it in businesses via stocks. This money represents their time and hard work. Therefore, when they put it into a company, they are putting in their “years of hard work” to help create or grow the company.

One may argue that if an investor buys shares from another investor, the second investor is not helping create or fund the company and therefore is not creating any value. There are two fallacies with this argument:

When an investor buys shares from another, the investor is elevating or maintaining the price of the stock. When the publicly traded company needs money and wants to get it from investors, it has a “secondary offering”, which is to sell stock on the stock market. The higher the share price, the more money the company can raise to fund its growth or R&D to create a new product.

Let’s say that you are an entrepreneur and you created a company that sells volleyballs. You risked your time and money to start the company. You took the risk in order to get reward. While you continue to own the company, you are taking all the risk that it might fail. Let’s say that you want to sell your company. An investor buys it from you. When this happens, you transferred all of the risk to the investor, but all of the reward should transfer to the investor as well. If the company does well and grows while under the investor’s ownership, the investor deserves all of the upside reward. Let’s say the investor sells the company to another investor, all of the risk and reward is transferred again. The second investor took on all of the risk by giving his/her money to the first investor. The second investor deserves all of the reward going forward. If the company continues to sell volleyballs, it is providing value to customers because the customers are getting value from the volleyballs. Therefore, both investors were providing value. The entrepreneur who started the company is no longer providing value.

Instead of buying and selling complete companies, such as the volleyball company, investors on the stock market are buying and selling portions, or shares, of companies. Therefore, they are responsible for a portion of the value that the company provides to its customers. To get into this position, many retail investors risked their life savings to do this. Quite often, publicly traded companies flounder or fail, causing investors to lose money. When companies do well, investors make money. This risk/reward ratio needs to be enticing, otherwise no investors would help companies grow and create new products.

So, if you are an investor in companies, via stocks, you risked your money, that you earned through years of hard work, in order to get reward. You will lose on some of your investments and win on others. You should be rewarded for taking the risk. When you are rewarded, you deserve it. On top of this, you are creating value by owning companies, which create value. If they didn’t create value, they wouldn’t exist.

Some investors make more money than other investors. This is usually because they helped companies (by investing in them) that created the most value. If you helped Netflix, you helped them create a ton of value for society. By investing in mainly companies that create the most value, you will make the most money. It makes sense because if you help provide a lot of value to society, you should make a lot of money. Also, this is in line with risk/reward. If you invested in Netflix when it was one year old (when Netflix needed investors the most), you would have taken much more risk and therefore should make much more money than if you invested in Netflix when it is 10 years old.

You should never apologize to anyone for being an investor. You are part of a system that creates most of the wealth for society. Without companies that create new products and services, our society would be dirt poor. We wouldn’t have most of the things that you see around you. Take a look around your room, your house, your street, your city and your country. Most of that wouldn’t exist if it wasn’t for companies. The majority of workers in the country wouldn’t have jobs and salaries if it wasn’t for companies.

Investors deserve every cent that they make. They enable companies to provide value, which help the economy provide value. The economy feeds everyone and pays for everything, including the government. The rich countries are rich because of their economies, which are made up of companies, which are created and funded by investors.

But, if you make money, others will feel entitled to it. They are wrong. They are not entitled to it. They didn’t take huge risks, by putting their life savings, which represents many years of hard work, into companies, which can go bankrupt or create a ton of value.

Even if you didn’t work or take any risks, they are not entitled to it. Let’s say you won the lottery. Am I entitled to your winnings? No.

But unfortunately, you live in a society where others will be able to forcibly take your money by voting in governments to do it for them.

They want you to take all of the risk, but they want a portion of the reward, by taxing you. When you earned your money from your job, you already paid income tax on that. Then when you invest that after-tax money and make capital gains, the government wants to take your money again. They take no risk, but take a lot of the reward.

You should be proud to be an investor, for helping create wealth for many people throughout society. The question should be: “Does the government create any or sufficient value for the money that they take?”

I’ve broken these rules a few times. When you lose X%, it takes more than X% to recover the loss. As an example, if you lose 20%, from $100 to $80, you need to make 25%, from $80 to $100, to recover the loss. If you lose 50%, you need to make 100% to recover. If you lose 100%, you can never recover.

I’ve lost 100% on more than one stock. This is because I was a victim of dishonesty. But I was largely to blame, because I fell for the dishonesty when I should not have. I invested in NIVS, which was a Chinese company purporting to be growing fast. This was verified by a relatively unknown auditor in China, which supposedly was a branch of an U.S. firm. The company’s website was of poor quality, which should have been a warning. Then the news of the fraud was reported. Stock was de-listed. Lawsuits were filed against the auditor, but there was no way to indict the company or its executives.

There were three warnings which I ignored:

Unknown auditor

Poor website

Little to no deterrence to lie, because the company executives are immune to penalty

There was no way for me to verify that this company exists, let alone that it is growing

I fell for their fraudulent growth story.

On another stock, I lost 100% when the company went bankrupt. This was harder to detect the dishonesty. In retrospect, I can see how the CEO did not tell us all of the bad news and the likelihood of bankruptcy.

If you can improve your skill to detect dishonesty, you will avoid losing money and be a much more successful investor.

The investing world is rife with dishonesty. Warren Buffett and Charlie Munger have complained about this for decades. There is a huge motivation to be dishonest: money. The dishonesty comes in many forms:

Lie

Lie by omission

Exaggerate

Spin

One of the common ways to deceive is with EBITDA (Earnings Before Interest Taxes Depreciation and Amortization). Buffett and Munger have complained about this. By not deducting depreciation and amortization, companies show higher earnings. The motivation to do this is to boost the share price. Since 50-90% of a CEO’s compensation is from stock or stock options, there is a significant motivation to boost share price. However, the effect from this is short term. No company can honestly avoid depreciation and amortization forever. These are valid expenses and should be included every year. To explain why, let us pretend that you own a lemonade stand and it costs you $100 to buy the table. The table will last 10 years, after which it will need to be replaced. Since the table is providing value to the business for 10 years, you are effectively spending $10 per year to put your lemonade on a table. This is depreciation. Let us suppose that your lemonade stand makes $20 profit per year, after deducting $10 depreciation per year for the table and cost of the lemonade from the revenue. You can boost your profit to $30 if you use EBITDA. On every quarterly report, executives push their EBITDA number to mislead investors.

Another common way to mislead is by excluding stock option (used to attract talent) as an expense. Again, this deception gives the impression that the company is making more profit than it really is.

Below is how I rank the sources of information, from least dishonest to most dishonest :

Audited financial statements from a reputable auditor (though this is not perfect, as Enron and Worldcom were able to defraud their reputable auditors)

Audited financial statements from a non-reputable auditor

Articles from news outlets such as CNBC, Forbes, Reuters, Bloomberg, Motley Fool

Analysts who disclose their conflicts of interest

Articles from Yahoo Finance, Zacks, SeekingAlpha

CEOs, CFOs

Articles from sources that you have never heard of before (This is not to say that their information is wrong. But you should try to verify it with another source. Minimally, this information is not audited like financial statements are.)

Commenters on discussion forums

Political articles from most sources. They lie, exaggerate, spin or twist incessantly. They are out of control.

Most of the above people have a motivation to promote or demote a stock, which is to MAKE MONEY. They own the stock and they want you and others to buy it as well, to boost the price. Or, they are short sellers who want the price to go down.

Not all promoters and demoters of stocks are dishonest. Many will tell you honest reasons why a company and its stock will grow. But CEOs, as promoters, are usually dishonest because they never give you both sides of the story. They never tell you the negatives of their company, especially if they are going bankrupt. If you believe them, you can watch your stock go to zero, as I have. Short sellers are usually the most honest. However, some can be dishonest as well to make a quick buck. They will write dishonest reports to attack a company and then make money in the following few weeks or months before the truth comes out. If you fall for these and sell your stock after it has dropped, you will lose money.

The mother of all liars are the media in regards to politics.

Noam Chomsky wrote “Manufacturing Consent” in 1988, which explained that the media lie to manufacture consent. Chomsky explained that the media lied about Gulf of Tonkin to manufacture consent for the Vietnam war.

Since 2008, the media have been manufacturing consent for Obama, Hillary and Biden. When they failed to manufacture a victory for Hillary, they have been manufacturing a defeat of Trump.

The media promoted lies from both sides of the political aisle: Republicans’ lies and then Democrats’ lies. One consistency is that the media lied for warmongers: Bush, Obama, Hillary and Biden. Obama/Biden dropped more bombs than Bush. Obama funded AQI, which exacerbated the Syrian war, which killed 500,000 and displaced 6 million. Later, AQI morphed into ISIS. Obama and Hillary helped kill 40,000 in Libya. Hillary’s campaign promise to stop Russia planes in Syrian air space increased the possibility of conflict with Russia. This common theme equates to war, which increases revenue for the media. Wars are huge revenue boosters for the media. Again, there is a motivation to lie: money.

In 2003, my friend laughed at me for saying the media lies. He was talking to me from a sports bar on March 20th, 2003, where many people gathered to watch the Iraq invasion. It was like a Super Bowl event, which as you know, is highly lucrative for the media.

Know that the media outlet does not have to do the lying. There can be people on two opposing sides, but the media will broadcast people from one side only. Phil Donahue questioned the Iraq invasion. MSNBC cancelled his show. Dr. Drew questioned Hillary’s health. CNN cancelled his show.

In 2016, the media published opinions from only one side, who told us that if Trump is elected, there would be an immediate crash of the economy and stock market. This included business news outlets, such as CNBC, Reuters, Marketwatch, Business Insider, Citigroup, Bloomberg, former chief economist of the IMF, Wedbush, Bridgewater, Macroeconomic Advisers and The Economist. Links to these are listed below. So, it’s not only the highly politicized mainstream media that lie about politics, but so do business media outlets and Wall Street.

If you believed the media, you would have missed out on a huge rally. In the past 4 years, from November 3rd, 2016 (Election Day) to November 8th, 2020 (Election Day), the S&P 500 went up 57%. The business news outlets are supposed to help their readers make money. Instead, they helped readers lose money. They didn’t care, as long as they can manipulate and brainwash voters.

The media have lied so much against Trump and to protect/boost Hillary and Biden, that it would take a book to show the examples. In fact, there are books about this, such as The True Story of Fake News. It is not surprising that the only time that the media praised Trump was when he shot missiles into Syria.

Even CNBC and 60 Minutes lie about politics. I have watched them for over 1-2 decades, but when it comes to politics, they lie. They referred to Hunter Biden’s hard disk as “unverified” multiple times. But it was verified by Hunter’s associates and Hunter’s lawyer. When the media pushed the Russia-Trump conspiracy theory for three years, which turned out to be one of the biggest lies in our lives, they never referred to this as “unverified”.

To detect dishonesty, you need to be willing to read information that goes against your bias. After your stock has made a lot of gains, you develop a bias for it. You can even get emotional and fall in love with that stock. When bad news comes out about it, you are averse to reading it, because it goes against your narrative and might show that you made a mistake and will lose money. You do not want something that will make you feel bad, so you do not read it. This is a big mistake, because you are not getting the full truth about the company unless you read both sides of the argument.

This proclivity to fall for one-sided, dishonest reporting is especially pronounced and prevalent in politics. Once you develop a bias, you seek out confirmation of your bias (“confirmation bias”) and are repulsed by information that goes against your bias. So you avoid it. Consequently, liberals are in one silo and conservatives are in another, as liberals consume CNN, MSNBC, New York Times, Washington Post, etc., but will not consume Fox, Newsmax, OAN, Breitbart, etc., and vice versa for conservatives (but less so). (Most of the media are liberal or leftist.) In Canada, liberals consume CBC and CTV and conservatives consume National Post and Rebel News. In my opinion, CBC is the most dishonest in Canada. As Matt Taibbi explained in his book “Hate Inc.: Why Today’s Media Makes Us Despise One Another”, there are major news stories that are reported from only one side of the media. So, if you consume news from only one side, you are not getting the truth.

If you were willing to consume news from the other side, you would have seen investors disputing the prediction that the stock market would crash if Trump won in 2016.

In 2002-2003, the media were promoting Republican lies. In 2003, I had to seek out a news outlet from the other side, to get the truth about Iraq. From 2008 until today, the media are promoting Democrats’ lies. If you want to know the truth, you need to seek out news outlets from the other side.

It is unlikely that you will detect all dishonesty. It is likely that I will fall victim again in the future. But the more dishonesty that you can detect, the more successful you will be in investing.

Media in 2016: Economy and Stock Market will Crash if Trump is Elected

“If the question is when markets will recover, a first-pass answer is never.”

“Under any circumstances, putting an irresponsible, ignorant man who takes his advice from all the wrong people in charge of the nation with the world’s most important economy would be very bad news.”

“So we are very probably looking at a global recession, with no end in sight. I suppose we could get lucky somehow. But on economics, as on everything else, a terrible thing has just happened.”

“economic consequences of Mr Trump’s presidency could be enormous, and costly.”

“Yet even if Mr Trump does not land America and the world in a serious new conflict or a global depression, his effect on the trajectory of global growth and development could be substantial and terrible.”

In Economics, there are Macro Economics and Micro Economics.

Macro Economics is the study of the economy, interest rates, inflation, money supply, fiscal policy, monetary policy, recessions, GDP growth, employment, etc.

Micro Economics is the study of decisions made by people and businesses regarding the allocation of resources, and prices at which they trade goods and services.

Similarly, there are different types of investors. I refer to them as Macro and Micro investors.

Macro investors trade in currencies, commodities and ETFs that track the broad market, such as the Dow, S&P 500, Nasdaq, TSX, FTSE100, etc., which are heavily influenced by the economy. They invest in banks, which are heavily influenced by interest rates. They invest in oil companies, which are heavily influenced by oil prices. They invest in cargo shippers, which are heavily influenced by the economy or international trade. They invest in gold miners, which are heavily influenced by the price of gold. They invest in mineral miners, which are heavily influenced by the economy. They invest in real estate, which are heavily influenced by government manipulation, such as CMHC, interest rate, RRSP mortgages, Cash for Caulkers, etc.

A common factor for Macro investing is that the investments are heavily influenced by external factors, such as the economy, interest rates, etc.

Micro investors invest in businesses.

Micro investors focus mainly on the business, its strength, weaknesses, opportunities and threats (SWOT). What is the competitive advantage (moat)? Why will the business continue generating and growing its revenue? Is it spending on capital expenditures (capex) so that it can grow? Is it spending on research and development (R&D) to create new products or services? Does it have good and honest management? Is it improving efficiencies and growing profit margins?

A common factor for Micro investing is that the investments are heavily influenced by internal factors, such as the company’s strength and weaknesses.

There are external and internal factors to both types of investments, but external factors have more weight to Macro investing and internal factors have more weight to Micro investing.

So, why choose Micro over Macro investing?

Because it is easier to predict the change and effect of internal factors than external factors. As an example, if a business came out with a new, revolutionary phone like Apple did in 2007, it is easier to see how this will increase Apple’s revenue. It is very difficult to predict how currencies, interest rates, government or the economy are going to change. It is very difficult to predict how OPEC is going to change oil prices. For some people, they might as well flip a coin. When Tesla came out with cars that are superior in almost every way to almost every car in the world, it is easy to predict that they will grow and have a prosperous future. How confident are you with your prediction about the direction of interest rates?

Macro investments have less control over their destiny. Houses cannot increase their value on their own. They need population growth and the government to keep interest rates low and to continue their price-boosting manipulation, such as insuring mortgages so that banks will lend out more mortgages, capital gains exemption, etc. Gold miners are at the whim of gold prices, which they have no control over. If you invest in an ETF that tracks the broad market, you are essentially betting on the economy and your ETF is at the whim of the next recession.

Micro investments have more control over their destiny. They care less about recessions. They build more factories to grow. They create new products, like Acuity Ad’s Illumin, Enphase’s grid-independent IQ8 or Tesla’s Cybertruck, to get more customers and generate more revenue. They expand to other countries, like Roku is doing.

This is not to say that you ignore external factors. The industry is still very important. Is the business in a growing or stagnant industry? Is the stock market in a bubble or over-sold? Is a pandemic coming around the corner?

It is possible to make money in either Macro or Micro investing. But it is easier, or less difficult, to make money in Micro investing. The empirical evidence supports this. There are rich Macro investors, such as Jim Rogers. However, the majority of the richest investors are Micro investors, such as Warren Buffett and Peter Lynch. Warren Buffett had said that he wouldn’t care if the Federal Reserve chairman whispered in his ear on what the interest rate will be next month. It would make no difference to how he invests.

Most of the business news on CNBC, Reuters and Bloomberg are only relevant to Macro investors. Micro investors can ignore most of it and save a lot of time, to spend on researching businesses, most of which will not be covered by business news outlets.

Macro investors are not necessarily bears, but in my opinion, most perma-bears are Macro focused. It is easy to be drawn into CNBC, Reuters and Bloomberg, which make money by getting viewers. Pushing greed and fear gets viewers. On a minute-by-minute basis, even on a weekly basis, the stock market is relatively uneventful. But, CNBC plays movie-like suspense music to keep you on the edge of your seat. Fearful viewers are bears. If bears are able to be Micro focused, they will transform into bulls.

When you buy most mutual funds or ETFs, you are Macro investing. This is because they hold so many stocks or securities that you are essentially betting on external factors.

As explained in ALLOCATE 100% TO STOCKS, I believe that investors should allocate 100% of their portfolios to equities. The main reason I gave is that equities outperform fixed income.

This is a very rare portfolio allocation. Most people in the world think this is too risky and will not do this. They allocate a percentage of their portfolios to fixed income to reduce risk, or what they think is risk. This is because they are looking at stock prices and not the business metrics. Most investors can tell you Apple’s stock price. They simply type in AAPL into their device or computer to get it. But they cannot tell you Apple’s revenue and never look it up.

Let’s say that you bought a lemonade company for $10,000. It has one lemonade-stand that makes $2,000 per year in sales. Every year, you make $2,000 in sales. This goes on unchanged for several years. During one of these years, somebody offers to buy the company for $15,000. Later, somebody offers to buy it for $3,000. Later, somebody offers to buy it for $10,000. Was it risky for you to invest in this company? Yes, if you look at only the offers from acquirers. It would be very volatile. When somebody offers $3,000, you might think that the company is worth only $3,000 and you might think that you lost $7,000.

But during this entire time, your lemonade company continues making $2,000 per year in sales. If you focused on this, would you think it was a risky investment? No.

Risk depends on what you’re looking at.

This is why Warren Buffett said he wouldn’t care if the stock market was closed for 10 years.

When people see their stock price go down to $3,000, they think they lost money. Hence, they think stocks are risky. But they haven’t lost $7,000. They’ve only lost it if they sell their stock. The drop in price might be warranted if the sales dropped sufficiently to justify a 70% drop. But if the sales hasn’t dropped, you simply ignore the $3,000 offer and go back to selling more lemonade.

Apple had a similar experience to the lemonade example. The stock dropped over 40% from 2008 to 2009, but the revenue and profit lines barely budged from its linear, upward trajectory. A good example, with charts, is given for Roku in FOLLOW BUSINESS METRICS, NOT STOCK PRICES.

People who focus on stock prices and people who focus on business metrics (Warren Buffett) have very different assessments of risk. People who focus on stock prices are looking at an illusion of risk. Stock prices alone do not represent the true risk of the investment.

Stock price volatility makes shareholders do things that owners of small businesses would never do, because owners of small businesses do not see offers to buy the company every day. Business owners are focused on running and growing their businesses, not on offers.

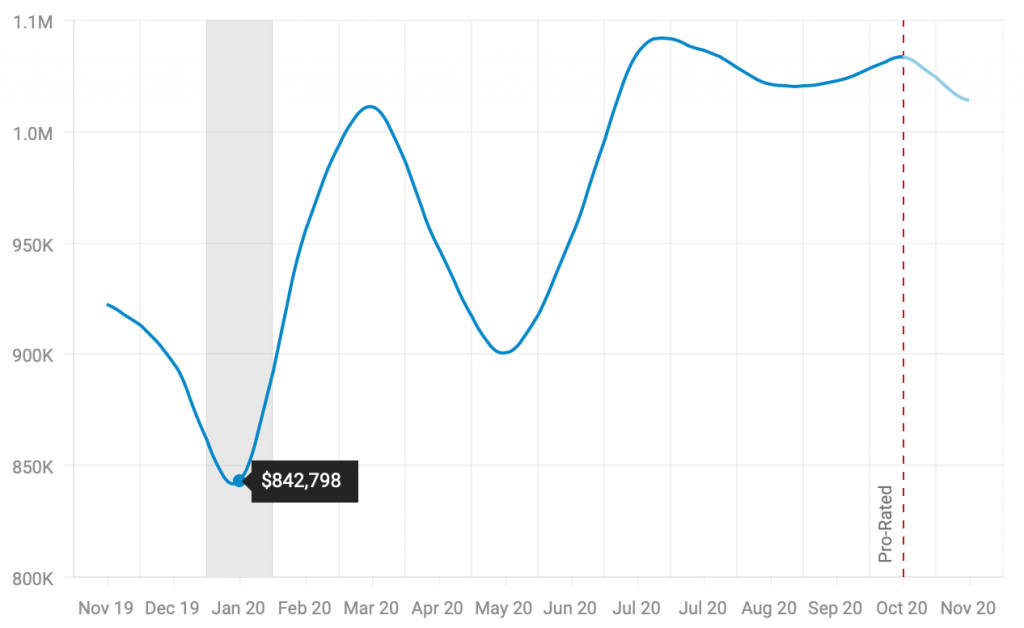

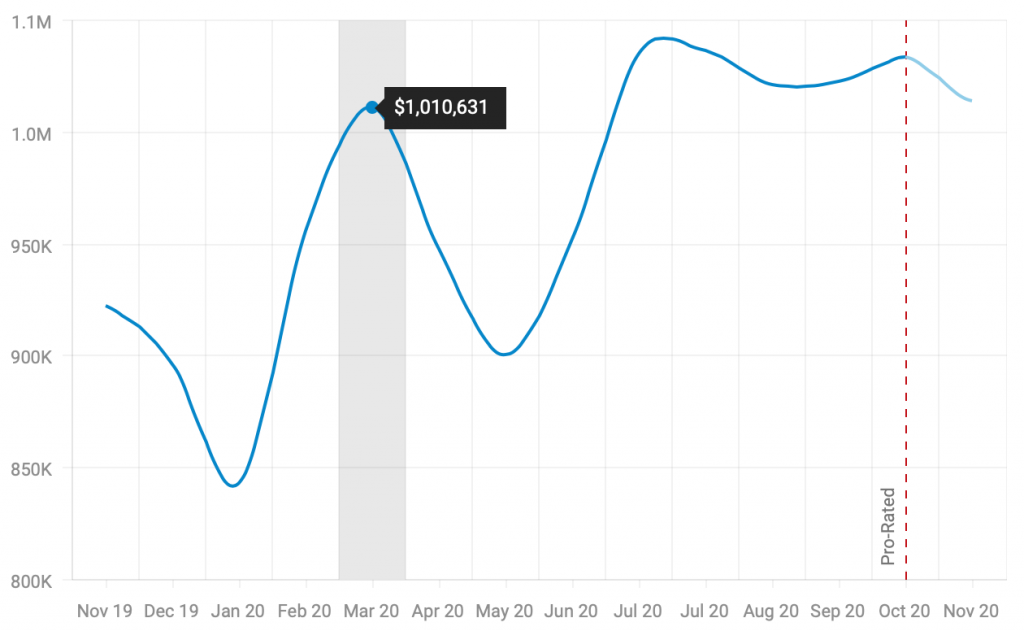

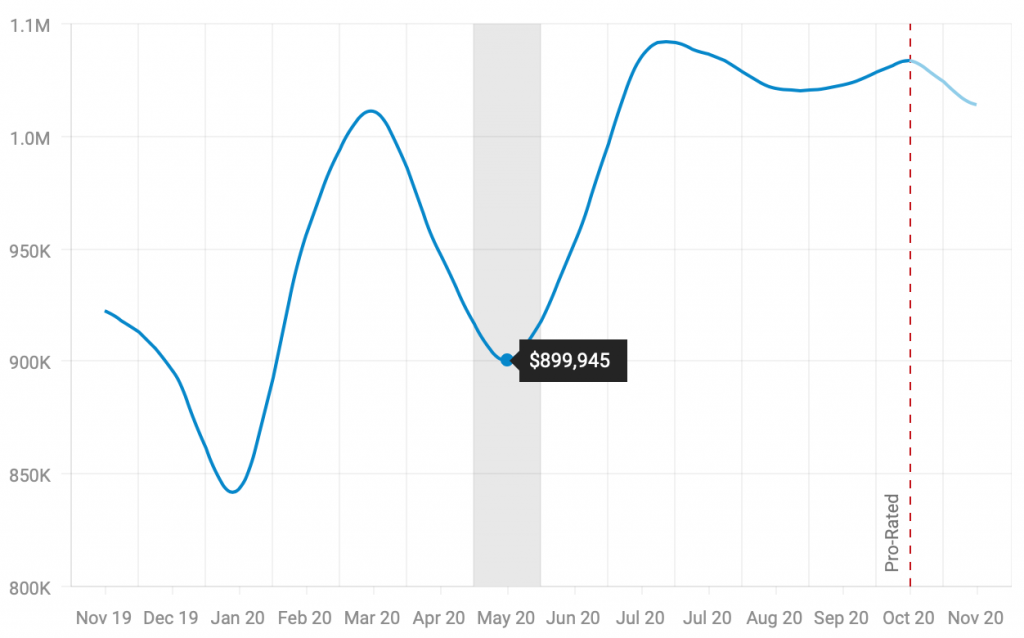

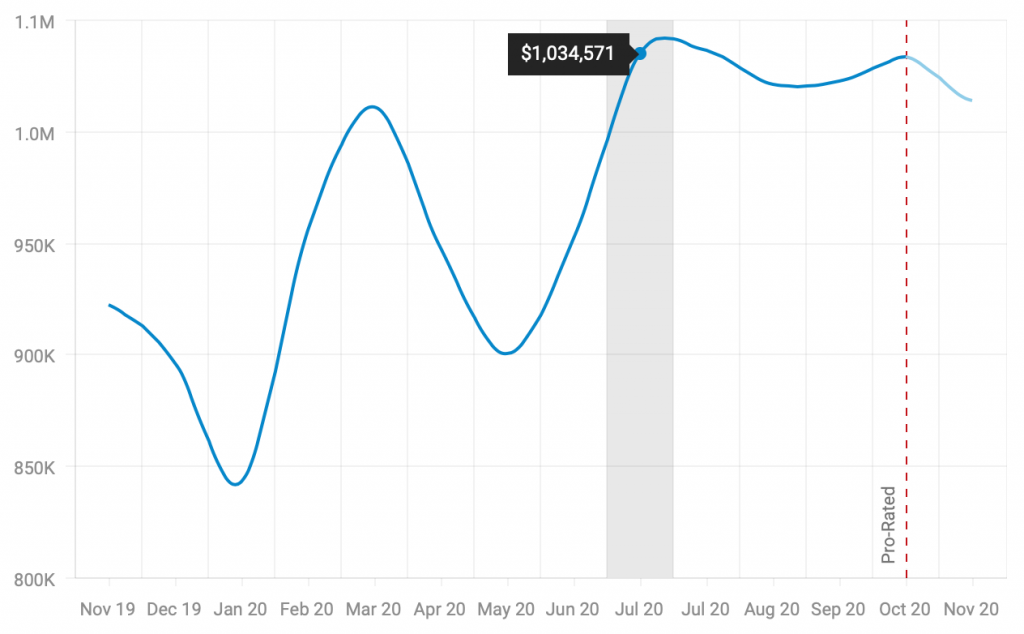

The stock market makes people think stocks are more volatile, and therefore more risky than other investments, such as real estate. This is also an illusion. Look at the price chart for Toronto houses.

Price changes from above chart:

Jan to March: +20% ($842,798 to $1,010,631) Mar to May: -10% ($1,010,631 to $899,945) May to July: +15% ($899,945 to $1,034,571)

That is just as, or more volatile than stocks. Why don’t people think real estate is as risky as stocks? Because people don’t check or get selling prices (offers on their houses) every day and these prices are not blasted to people every day.

Many say that your age should represent the percentage allocation to fixed income. Warren Buffett is 89 years old. Therefore, 89% of his portfolio should be allocated to fixed income. However, nearly 100% of his portfolio is in equities. His portfolio is essentially his ownership in Berkshire Hathaway, which in turn owns mainly equities in the form of complete ownership of businesses. The main reason Berkshire Hathaway might have cash or fixed income is because its business holdings generate so much cash that he cannot find enough businesses to buy and fast enough.

Ideally, you should do what Warren Buffet does, which is to buy out complete businesses, such as See’s Candy, Nebraska Furniture Mart or Clayton Homes. But most of us cannot afford to buy 100% ownership of a business. Stocks enable us to buy a portion (share) of a business, which is second best. Stocks enable anyone to be a business owner.

You should not think of yourself as an investor in stocks. You should not be a stock trader. You should be an investor in businesses. You need to put on your “business owner” cap and think like a business owner. Business owners make the most money because they have the best assessment of risk. Stock owners, who have an incomplete picture of risk, inevitably become stock traders and will usually underperform.

Peter Lynch is one the most famous investors in history. He outperformed Warren Buffett by averaging a 29.2% annual return from 1977 to 1990. In addition to other investment books and videos, I read Lynch’s books and I watched his videos. I was amazed by his number. At the time, it seemed impossible to reach Warren Buffett’s number, which is approximately 20%, let alone Lynch’s 29.2%.

In a way, I cannot believe that I reached that number.

The portfolio has been on gang busters in the past couple of years. Today, it hit a new milestone. It hit 30.3% CAGR (compound annual growth rate) or average annual ROI (return on investment). This is for the period from July 2008 until today, October 7th, 2020. Again, this does not mean that the portfolio grew by 30.3% every year. Some years were flat or negative. Some years were more than 30.3%.

As I have mentioned before, stocks do not go in a straight line. Next year, my CAGR may drop…or it might go up. Who knows. But the secret is to focus on the companies’ business metrics, not the stock prices and if the business metrics are doing well, the stocks will also do well.

The stock market does not wait for the economy to bottom before it rebounds. Usually, the market rebounds a few months before the economy does.

As with many other investors, I have been waiting for a treatment, cure or vaccine before I would jump back in.

First, there was anecdotal evidence of positive results from HydroxyChloroquine with Azithromycin. However, there were also reports that it has negative side effects or that it may not work as well as first thought.

In addition to the above, there are over 30 treatments and therapeutics being worked on.

I do not have 100% certainty that there will be a home-run treatment. However, there are likely going to be a number of treatments that will treat different patients with different situations or pre-conditions.

Therefore, I think that the death rate will decline. The pandemic will likely slowly improve from this point on. It will not go back to normal anytime soon. It likely will take one to two years. But if you wait for everything to go normal, then you might miss out on opportunities to buy stocks cheaply.

Also, there are many companies working on a vaccine for SARS-CoV-2. Therefore, the probability of a vaccine coming out is greater than one coming out for MERS or SARS. There is even this:

The majority of these companies working on treatments and vaccines will fail. But because there are so many, there is a better probability of a company coming out with something for SARS-CoV-2 than for other viruses.

Therefore, I jumped back into stocks today.

Of course, I could be wrong with any or all of the above. There could be collateral damage that surfaces later on, that I cannot foresee, such as a credit crisis because so many consumers might stop paying their mortgages or credit cards. Corporations are heavily indebted as well and might start a domino of defaults. The chances of this happening is low, due to the trillions of dollars that the Federal Reserve and the U.S. federal government are pumping into companies and individuals. But there is still a chance of this or other collateral damages.

But there is never certainty when investing in anything.

Roku streams TV channels, movies and digital content such as Netflix, YouTube and Prime. It enables consumers to cut the cord. People get Roku mainly when they buy new TVs, which has Roku pre-installed, or less frequently when they buy Roku devices.

I had suspicion that as more people lose their jobs, they would buy fewer TVs. I questioned the amount of money that advertisers would spend to advertise to people with no income and stuck at home. Consumers are not driving, taking vacations and going to restaurants.

However, Roku released information about their users’ viewing pattern:

The above announcement pertained to first quarter of the year, ending in March. Most of the “stay at home” orders will likely stay in effect until end of April or sometime in May. This will likely continue increasing usage of Roku.

I still think there is a possibility of a recession that lasts longer than what the stock market seems to indicate with this recent rally. If it does, it will have a material impact on Roku’s revenue. In which case, I might sell Roku again.

People should know that short term trades such as this are extremely difficult to make, and not recommended. There is a probability that this trade will become a losing trade. For most people, it’s better to buy and hold good businesses that will normalize in a few years and go on to new highs. Buy and hold is much easier than dealing with short term volatility. On the other hand, nobody knows if we will have a bear market and how long that lasts.

The stock market correction started on February 24th. We were busy preparing for and then flew to Hawaii for our vacation. It was surreal to watch this doom-filled volatility from the beautiful, sun-lit hotel pool in Hawaii with tall palm trees all around.

A couple of days later, the stocks bounced. Nevertheless, I told my wife that this is going to be worse than 2008, but it will not go in a straight line. There will be many “head fakes”, “sucker rallies” and “dead cat bounces”.

Fast forward to today and we have a full blown crisis, where both the U.S. and Canada had announced aid packages:

White House pushed for $1 trillion package.

Canada announced $82B aid package.

These will not be enough. It’s likely that these governments will increase this or announce another package.

This recession is going to be worse than the 2009 recession. Here is what caused the 2009 recession:

U.S. government enacted CREA (Community Reinvestment Act), which pushed banks to lend to low-income borrowers, in order to increase home ownership.

Fannie Mae and Freddie Mac bought mortgages from banks, in order to get banks to lend out more mortgages. They ended up with half of the country’s mortgages.

Wall Street jumped on board and sold mortgages to earn commissions. They sold to high risk, low-income borrowers because Wall Street was not the lender and therefore didn’t take the risk.

This fuelled the housing bubble.

Bubble burst

Homeowners stopped paying banks.

Banks were on verge of bankruptcy and stopped lending.

Tightening credit caused recession.

What most people do not realize is that it was the government that created the housing bubble and ultimately the crash and recession. The bail outs of Fannie Mae and Freddie Mac were much bigger than for AIG or the banks.

Consequently, the stock market dropped by as much as 10% in day, on multiple days.

During this deep recession in 2009, credit was tight, but people were still able to consume or produce. In May, 2009, Hawaii was dirt cheap, so my wife and I took a 10 day vacation for $2,200, which included hotel and flights.

This recession is much more different. Even if Hawaii vacations are selling for $100, you cannot buy one. People are told to stay home, self-isolate or stay in quarantine. Borders are closing. You cannot fly to Hawaii from Canada even if you offered $1 million to the airlines.

In 2009, you still saw people in restaurants, bars, movie theatres, etc. Today, you see no one.

In 2009, people still bought TVs, computers, electronics, etc. Today, Apple’s stores are closed.

The stock market has already dropped by 10% in a day, on multiple days.

In 2009, once credit loosened, the economy could recover. Today, the virus is still growing exponentially. To slow this down, the government is clamping down the people, which is clamping down the economy. If the government lets people go back to normal activities, the virus will flare up again, which will prompt the government to clamp people down again. This can happen repeatedly until the vaccine comes out in 12-18 months. Until the vaccine comes out, the economy might be kept in a coma.

In addition to the devastating impact on health and lives, this virus will wipe out trillions of dollars of wealth around the world. Bankruptcies will soar. Millions of jobs will be lost. The number of people on welfare will go up.

The crisis will eventually subside. Things will eventually go back to normal, once the vaccine comes out. Social distancing is going to be very boring. During this process, you will become poorer. To prepare, make sure that you have a budget and have enough of a buffer to pay for several months of expenses.

Note that the aid packages will come from you. You will pay for them. The government cannot create wealth. It can only take it from you to give to somebody else. Therefore, the country’s wealth will be the same as without the aid packages, and the country will still be poorer than before the virus.

Governments will likely bail out companies. Despite being an investor and shareholder, I object to this, and so should you. Many of these companies, such as the airlines and Boeing, were making billions of dollars of profits for many years. Instead of stashing this money into their bank accounts, they used it to buy back shares. This juiced the stocks, which benefited shareholders, but more importantly, it increased the executives’ stock options and bonuses. Now that their companies are losing money, their companies should sell shares to raise money. That’s the main purpose of the stock market: enable companies to sell shares to raise money.

If governments bail them out, they will be “Privatizing Profits and Socializing Losses”.

Some people might blame capitalism for these bail outs. This is socialism, not capitalism. Capitalism advocates that incompetent businesses should die and disappear. Socialism advocates that governments help businesses. “Socializing Losses” is socialism.

Similarly, the problem with Wall Street in 2009 was socialism, not capitalism. Bailing out Wall Street firms is socialism. Furthermore, it was the government that created the housing bubble. (Similarly, Canada’s government created its housing bubble, but that is another long discussion.)

Some people might argue that compensating executives with stocks is the source of the problem. I disagree. If the government does not intervene with bail outs, these executives will learn the hard way for their mistake of stock buy backs and for not stashing enough money in the bank. Now that their stock price is low, these executives will not make bonuses. When they get their company to sell stock, they will continue to forgo bonuses, but they will prevent their company from going bankrupt.

This is the punishment and lesson that executives should endure and learn, but will not if the government bails them out.

You, as a taxpayer, should not pay for their mistake of not stashing their profits into their bank accounts.

Even if you bail out these companies, it does not prevent them from declaring bankruptcy. Governments forced taxpayers to give billions of dollars to GM in 2008. It still declared bankruptcy anyways.

I’ve been following the reports on this virus for the past 3 weeks. Since early February, I felt that this would cause a correction but was surprised that the market was ignoring it.

Then I got busy getting ready for my vacation to Hawaii and flying there when the correction started.

Yesterday, I got some time here in Hawaii to research this more. Today I sold my stocks.

It looks like the WHO (World Health Organization) and several countries have been lying about the severity of this virus. China, Thailand, Vietnam, Iran and the U.S. likely have multiple times more cases than they are reporting.

The U.S. has only reported 50-60 cases, all of which came from travellers from the Diamond Princess cruise ship or China. Yet, California has thousands in quarantine. Today, the first case is reported where the source of the infection is unknown. This implies that it is spreading within the U.S. and many more will be reported in the future.

Iran and Thailand likely have tens of thousands of cases.

This virus is much more infectious, easily spread and deadly than either SARS or the flu. People are succumbing and falling on the ground in some countries. Victims can get sick more than once. Contagious period can be up to 27 days without symptoms. Another difference is the size of the Chinese economy compared to when SARS broke out. This means that the impact to the world economy will be much more significant.

China has been shutting down almost entire cities. This will disrupt supply chains that the world depends on, which in turn will slow the world’s economy.

CDC has said that a pandemic is essentially assured. Germany said that they will have an epidemic. Europe is not doing enough to contain it. The U.S. is not doing enough testing. Italy is using the military to quarantine victims. There are long lineups at the grocery stores in South Korea and the shelves are empty in stores near the cluster in Italy. The number of cases worldwide are doubling every 4-5 days. Vaccine is one to one and a half years away. It looks like it is going to get worse before it gets better.

There is a possibility that this might be the start of the next bear market or recession. Hopefully, I’m wrong.